This fall, a federal judge in Jackson ruled that Mississippi is not providing community mental-health services that comply with federal law. What’s perhaps less well-known is how egregiously the private sector fails to meet those same federal standards.

If you think lack of access to mental-health services is only an issue for people on Medicare or Medicaid here in Mississippi, think again.

Mental healthcare is not something you miss until you need it. If you have a steady job at a stable organization, it’s easy to think you have all the essentials covered for your family. Health plan, 401(k) — dental and vision coverage, even.

But what happens when your 20-year-old daughter, who’s always been physically health, gets swallowed up by anxiety and depression as a college student?

The stakes couldn’t be higher. More than 1 in 7 young adults develops a substance use disorder; it often begins though self-medicating their mental-health struggles. And every year, more than 100,000 young adults die by suicide.

As terrifying as the potential outcomes of mental illness can be, the reverse is also true: Excellent outcomes are likely with appropriate treatment.

Getting your child seen by a psychiatrist and having her work with a therapist not only allows her to survive through today’s crisis; it also equips her with healthy coping strategies to face her future challenges.

Appropriate mental healthcare, done early and done well, can redefine the course of a young person’s life.

Unfortunately for people in Mississippi, many insurance companies cover only enough outpatient care to avoid the first scenario — but not enough to actually treat mental illness appropriately.

Many insurance companies continue to look at mental health as an “extra.” This is despite a 2008 federal law which says they cannot cap benefits for mental and behavioral healthcare differently from medical and surgical care.

On the other hand, however, are those insurers who understand that mental healthcare is an aspect of basic healthcare. They also understand a fundamental healthcare principle: Early intervention controls costs in the long run.

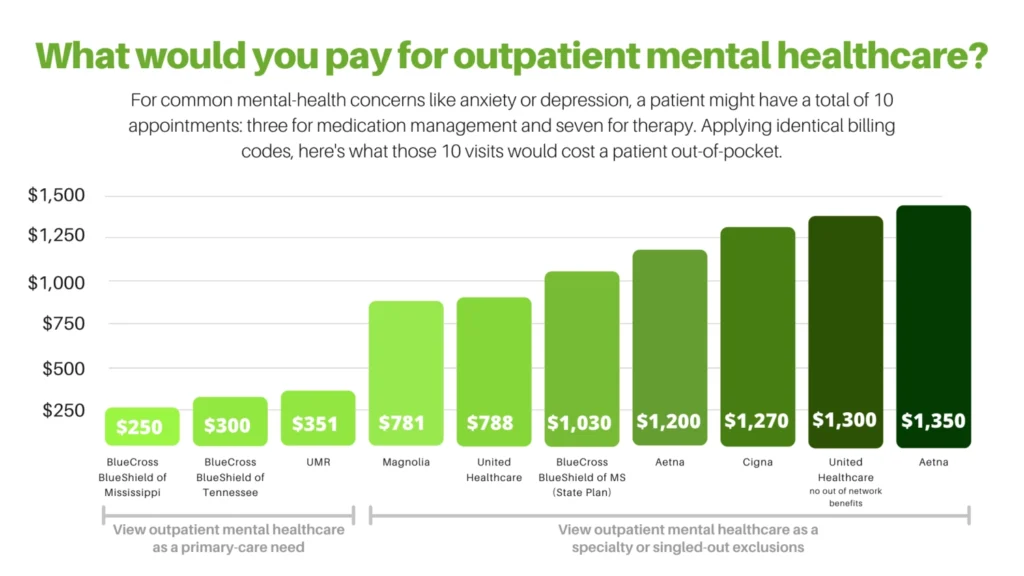

BlueCross BlueShield of Mississippi is the best example in our state. The coverage it provides for outpatient mental healthcare is the gold standard. BCBS of Mississippi covers outpatient mental-health visits as primary care; for most people, this means a simple copay of $25 to $35 per visit.

In contrast, plans like Cigna, Aetna and United Healthcare create financial barriers for patients in several ways. They classify outpatient mental-health visits as a higher-cost “specialty” visit. They set reimbursement rates so low — often less than a third what BCBS-MS provides — that psychiatrists and counselors do not join their network. Then they steer patients to “in-network” providers for mental healthcare, chiefly primary-care physicians who are not trained in psychiatry. The psychiatrists who are in-network are limited, and the wait time to see them may be four to six weeks.

In simple terms, people who have these plans cannot access outpatient mental healthcare without having to pay a large amount out-of-pocket.

We looked into our own billing data to quantify exactly what this means for patients. Someone struggling with anxiety or depression might need 10 visits over three months, including medical and therapy visits. If they have BCBS-MS insurance with a $25 copay, these 10 visits would total $250 out-of-pocket. But if they have United Healthcare, for example, they would pay $788 (in-network) to $1,300 (out-of-network) for the exact same course of treatment.

Why do insurance companies create these kinds of barriers to mental health? It’s not because there is outcome data behind it. You know as well as I do, it’s simply a way to save money.

This is the same reason why companies choose these plans to offer to their employees. Do they save money? Sure. And they do it by singling out mental-health services for restrictions, flaunting parity laws in the process.

“When you prevent people from accessing care at the outpatient level, all it does is spell higher costs down the road.”

The true cost comes to light when you consider that one in five adults is living with a mental illness. When you prevent people from accessing care at the outpatient level, all it does is spell higher costs down the road. Businesses and families both suffer when mental-health concerns escalate and people cannot work or have to be hospitalized.

As long as Mississippi allows these insurance plans to continue operating in the state, it will be up to employers and employees to look more closely at their plan’s costs and benefits.

It’s not just about the deducible and the copays. Does the plan treat mental-health visits as primary care, instead of more-expensive specialty visits? Are any credentialed mental-health professionals in your area in-network?

If not, you might find out too late that what seemed like “good insurance” only has you covered from the neck down.

Billy Young has spent more than 40 years in mental and behavioral healthcare. He is CEO of Right Track Medical Group, a network of outpatient mental-health clinics in North Mississippi.

Our Biloxi Location Has Moved!

Right Track Medical Group is now serving patients at our new location:

1633 Popps Ferry Road, Suite A

Biloxi, MS 39532

We look forward to welcoming you to our new office!